Silicon Valley still hasn’t completely recovered from the scars from the heyday of Webvan and Pets.com. When the software industry started to gain momentum, investors considered another bubble and gave their opinion. Many new internet companies like Facebook and Twitter started sparking controversy in the Silicon Valley. We all know how the dot-com bubble companies plunged in the early 2000’s came into play. However, the software companies are very different from such internet companies.

Marc Lowell Andreessen ( an entrepreneur, investor and software engineer ) believes that many of the prominent new internet companies are building real high-growth, high margin, highly defensible businessesMark says that software cannot be considered a bubble because it has changed the world how it operates over the past 50 years. Today looking around we all can agree that everything has an ever-growing presence of software.

Software programming and internet services have made launching start-ups easy, due to lower cost requirements. The cost of running an internet based application has reduced to one-tenth of what it was about a decade ago.

Today the world’s largest bookseller, Amazon, is a software company. The largest video service by number of subscribers is a software company: Netflix. The dominant music companies are software companies, too: Apple’s iTunes and Spotify. Today’s fastest growing companies are videogame companies like Zynga (maker of games like Farmville). LinkedIn a software company is today’s fastest growing recruiting company.

Software is also eating much of the value chain of industries that are widely viewed as primarily existing in the physical world. This shows the dominance software has obtained today.

The article concludes by saying that software companies had successfully survived the period of an economic slowdown. This gives the indication that they can grow even more in future. Instead of constantly questioning their valuations, let’s seek to understand how the new generation of technology companies are doing what they do, what the broader consequences are for businesses and the economy and what we can collectively do to expand the number of innovative new software companies created around the world. The changes brought about by software will affect jobs and people need to enhance their skills, be aware of the changes brought about by software and accept the changes to still have a value-oriented job in the coming future.

Pat Dorsey is a CFA charterholder. He holds a Master’s degree in Political Science from Northwest University and a bachelor’s degree in government from Wesleyan University. He is the founder of Dorsey Asset Management. Prior to starting Dorsey Asset, Pat was Director of Research for Sanibel Captiva Trust, an independent trust company serving high net worth clients. From 2000 to 2011 Pat was Director of Equity research for morning star.

Chapter 1: The Five Rules For Successful Stock Investing

Do your homework: Investors usually make the mistake of not thoroughly researching the company before investing. To know the situation of the company, you must have an understanding of accounting. This is very important because you can spend time reading the annual report, understand the competitive landscape, research past financial statements, or do research about the company and uncover a lot. Unless you know a business inside out, you shouldn’t buy a stock.

Find Economic Moat: Economic moat basically prevents competitors from attacking a company’s profits. Economic moats allow a relatively small number of companies to maintain above-average returns over the years, and these companies are often the best long-term investments.

Have a Margin of Safety: Margin of safety is when you buy a stock at a price lower than its intrinsic value. The future is so uncertain that additional cushions are needed in case the situation is worse than expected. Adhering to valuation discipline is very important because losing money is much more painful than not making money.

Hold for the Long Haul: Never forget that buying a stock is a major purchase and should be treated like one. If you trade frequently you’ll rack up commissions and other expense that over the time gets compounded. It also dramatically increases the taxes you pay. Thus, pick the investment carefully and then stick to it unless it is better to sell than hold.

Know when to sell: You shouldn’t sell just because stock has dropped/skyrocketed. Share price movements covey no useful information because they can move in all directions unreasonably in the short term.

Whenever you think you need to get out a stock, ask yourself these questions:

Do you have too much money in a stock?

Have the fundamentals deteriorated?

Are there better opportunities?

Did you make a mistake buying it in the first place?

Has the stock risen too far above its intrinsic value?

Chapter 2: Seven Mistakes to Avoid:

People who lose money in the market are more than people who make money. Therefore, it is very important to know the financial mistakes investors make in the market. Here are seven major mistakes investors make:

Swinging for the fences: Loading up your portfolio with risky, all-or-nothing stocks is a sure route to investment disaster. One cannot estimate which company will be the next Microsoft in its initial years and also small growth stocks are the worst-returning equity category over the long term.

Believing that it’s different this time: When someone utters the words “it’s different this time”, run because history does repeat itself, bubbles do burst, and not knowing market history is a major handicap. The key is that you have to be a student of the market’s history to understand its future.

Falling in love with product: Great products do not necessarily translate into great profits. When you look at the stock, ask yourself, “Is this an attractive business?” “Would I buy the whole company if I could”. If the answer is NO, give the stock a pass, no matter how much you like its products.

Panicking when the market is down: It’s very tempting to look for validation when you’re investing, but history has shown repeatedly that assets are cheap when everyone else is avoiding them. The gains will be better if the company is studied, valued, and then invested rather than buying the stock of the month in the newspapers.

Trying to time the market: It is one of the greatest myths of investing.

Ignoring valuation: The best way to mitigate your investment risk is to pay careful attention to valuation because buying a stock on the expectation of the market or positive news flow can lead to the risk of losses.

Relying on earning for the whole story: In the end, cash flow is what matters, not earnings. Because earnings can be easily manipulated as compared to cash flows. You can spot a lot of blow ups well in advance, if you pay attention to operating cash flows relative to earnings.

Chapter 3: Economic Moat:

Economic Moats are the advantages that businesses hold which give them an upper hand compared to their competitors. These economic moats give the company a riding position and ensure future stability with the constant generation of cash flows. Thus, it is very important to know whether a company has economic moats.

Analysing a company’s economic moat

Analyse the competitive structure of the industry. How do firms in the industry compete with each other.

Has the firm been able to generate superior ROAs and ROEs historically?

If yes, what is the source of its profits? Why is the company able to keep competitors from stealing the profits?

Estimate how long the firm will be able to hold off competitors.

Evaluating profitability

Calculate ROCE and ROE.

How much free cash flow does the firm generate?

Calculate the firm’s free cash flow as percentage of its sales.

Calculate its Net income as percentage of its sales.

Companies that continuously produce robust ROE, free cash flow and adequate margins are much more likely to have a truly economic moat. However, many sophisticated ways to measure an economic moat are to calculate the ROIC (return on capital) that a company creates in excess of its weighted average cost of capital (WACC).

Real product differentiation through superior technology or features.

Perceived product differentiation through branding and reputation.

Driving costs down and offering the product at lower price.

Locking in customers by creating high switching costs.

Locking out competitors by creating entry barriers and success barriers.

Chapter 4: The Language Of Investing

A balance sheet is like a company’s credit report because it tells you how much a company owns compared to its liabilities at a particular point in time.

The income statement tells how much the company made or lost in accounting profits during a quarter or a year. The income statement records revenues and expenses over a set period, such as fiscal year.

Finally, there is a cash flow statement that records all cash coming in and out of the company. The cash flow statement connects the income statement and the balance sheet together.

Why need of P&L account and cashflows statement? – To setoff impact of accrual accounting. If Britannia produces and sells biscuits faster than its customers pay for the biscuits, sales growth would look fantastic even though cash is flowing out the door – which is why we need a statement of cash flows.

This is the crucial difference between accounting profit and cash profit. Accounting profit matches revenue and expenses as much as possible, while cash profit measures only the actual money that go into and out of the business.

The difference between accounting profit and cash profit is important for understanding almost everything you know about how your business works and how to separate good and poor businesses.

Chap 5: Analysing a Company’s Financial Statement:

Equity represents the value of money that shareholders have invested in a company. The basic equation for the underlying balance sheet is:

Assets – Liabilities = Equity

Chap 6: Analysing a Company- The Basics

Five aspects to analyse the company:

Management

Profitability

Financial health

Growth

Risks / bear case

Chap 7: Analysing a company – Management

Good management can make poor business bigger. Bad management can make good business poor. Therefore, you should always analyse the management when buying stocks. Here, the authors divide the management evaluation process into three parts:

Compensation: A manager’s remuneration must be neutral or linked to the company’s net income. Not too high or too low. If the manager achieves the goal, then compensation should be higher.

Character: In a company we should check if there is any related party transaction? Is the board filled with managements family? Does the management provide enough information to properly analyse the business?

Operations: Does the management allocate its cash efficiently? Is the management diluting too much equity? Do the actions of the management match with what they claim to do?

Chapter 8: Avoiding Financial Fakery

Financial Fakery refers to a deceptive accounting technique used to misrepresent the value of a company, thereby giving an investor the financial incentive to invest in a company. Financial Fakery is nothing new. Most businesses can misrepresent and manipulate some accounting. One needs to be aware of whether this falsification is to a large extent. Here are 6 red flags to watch out for:

Six major red flags to thoroughly check:

Accounts receivables growing faster than sales.

Changes in Credit terms.

CFO or Auditor leaving the company.

Frequent acquisitions.

Cash flow from operations growing slowly as compared to sales.

Frequent one-time charges and write-downs.

Chapter 15: Consumer Services

Most of the economic moats for retail and consumer services sector are extremely low. The only way a retailer can earn a wide economic moat is by doing something that keeps consumers shopping at its stores rather than at competitors by offering unique products or low prices. It’s rare to find a retailer or consumer service firm that maintains any kind of economic moat for more than a few years.

Restaurants

For the sake of simplicity, restaurants can be divided into quick service restaurants (QSR FAST FOOD) and full service restaurants.

Demographic change and changes in the workforce make the long-term prospects for restaurants quite rosy, since in many households both parents work, there is little time left for cooking and even less time for shopping and cleaning.

Most new restaurant concepts begin in a speculative growth phase in which managers assess the growth potential for expansion. Many concepts fail, such as the term SPECULATIVE GROWTH.

In a period of aggressive growth, restaurants per unit must be profitable to support new store openings. It is spent so quickly to open business that it eventually leads to negative free cash flows.

Due to the rapid expansion, many times more money is required than the company generates internally. Thanks to operating leases, which are similar to renting space, you often help to finance your branch expansion. However,

Slow-growing restaurants tend to have strong free cash flows, high ROI, and generally pay dividends when they run out of business investment opportunities.

Retail

Retail is one of the sectors having a large number of people working the value chain. Retail is an inseparable part of the economy in modern times.

Over last decade, traditional department stores have become dinosaurs. Big stores such as Wal mart have stolen thunder of traditional department.

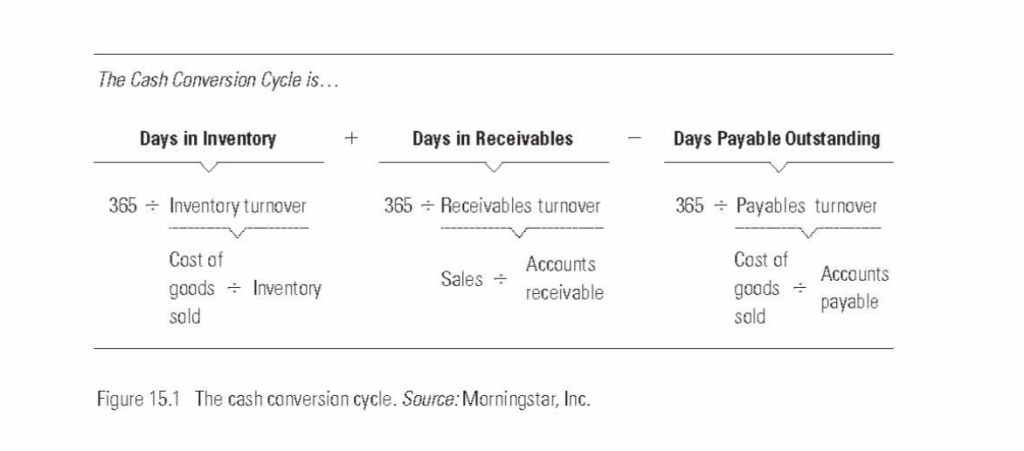

One of the best ways to distinguish excellent retailers is by looking at their cash conversion cycle.

The cash conversion cycle is a metric that expresses the time (in days) it takes a company to convert its investments in inventory and other resources into cash flows from sales.

Hallmarks of Successful Retailers.

First impression is the last impression.

Keeping an eye on store traffic.

Having a positive employee culture.

Chapter 23: Consumer Goods

Consumer goods consist of all items we see around us- Red label tea to Britannia biscuits to Harpic cleaner. The consumer goods sector is composed of industries such as food & beverages, household and personal products, and tobacco. The consumer goods sector is also a mature sector. Growth in this sector is slightly equal to GDP growth. Despite slow growth, stocks tend to be very lucrative.

How Companies Make Money in Consumer Goods

Consumer goods companies generate profits the old-fashioned way. They make products and sell them to customers, usually supermarkets, mass merchandisers, warehouse clubs, and convenience stores.

The beverages companies offer a slight twist in the equation by selling their products to distribution channels: bottlers and beer distributors. For example, nonalcoholic beverage firms such as Coca-Cola and PepsiCo manufacture the concentrate and syrups for the finished soft drink products and sell them to their bottling partners, who mix them with other ingredients, package the finished product, and sell it to retailers.

Key Strategies for Growth

Steal share from competitors, usually by introducing new products.

Acquiring other companies and increase the market share.

Reduce operating costs

Sell product overseas

Things for Investors to Watch Out For

Increasing power of retailers

Litigation risk

Foreign currency exchange risk

Expensive stocks

Economic Moats in Consumer Goods

Economies of scale

Big, powerful brands

Distribution channels and relationships

Chapter 24: Industrial Materials

Industrial materials include a wide variety of products, such as something as small as a bar of soap, JBL machines and rocket launchers, including all the items that require heavy industrial production for the products to be ready for sale / use. The sales and debt ratios are very important to analyse the companies in this industry. However, commodities tend to suffer from long-term price deflation. There is constant competition in the industry with low costs and overcapacity.

As the industry nears a cycle low, companies begin cutting costs, laying off workers, delaying production and resuming capacity as the business cycle advances. However, limited pricing power makes it difficult for industrial companies to deal with changes in demand. and excessive competition.

Basic Materials

Some commodity-producing companies achieve the low-cost position by increasing their size and achieving economies of scale. As a result, the unit production cost is lower than that of the competition.

In many sectors, such as the steel industry, domestic companies are increasingly coming under pressure from foreign products with a significantly lower cost structure. Their cost advantage generally comes from a combination of three sources: the sheer advantage of geographic location, government subsidies and tariffs, or low labour costs.

Although the basic industries have considerable barriers to entry, the costs for building a new steel, aluminium or paper processing plant are very high, and price competition brings at best mediocre profits.

The high cost of equipment and low profit margins mean that these industries generally have poor ROI, so there is little to attract investment capital and even less to attract investors.

Industrial Materials

Despite the many drawbacks this sector brings, there have been a few companies with few economic ditches that have turned these good companies into good investments.

The moats include high customer switching costs and patented technology.

Technological and Competitive Advantages

Hallmarks of Success in Industrial Materials

The Total Asset Turnover (TATO), one of the most frequently used measures of efficiency, is an easy-to-calculate ratio: annual turnover divided by total assets.

As a rule of thumb, a TATO index greater than 1.0 is quite good for an industrial company; Such an index means that for every dollar the company has invested in assets, the company will generate at least one dollar in income each year. .

The popular efficiency indicator is the asset turnover (FATO), which corresponds to the annual turnover divided by the net assets.

The FATO index is even more informative for industrial companies than the TATO, as industries are heavily dependent on real assets.

Most industrial companies have high operational leverage, which means that most of their costs are fixed regardless of volume and revenue.

Red Flags:

Debt

Pensions

Acquisitions

Chasing Market Share

To identify the industries with the best long-term fundamentals in the Industrial Materials sector, find out which industries have already seen significant consolidation. Then look for a cheap producer in comparison to domestic and foreign competitors and check whether they are in excellent financial shape and have additional income. Streams of value-adding products or services that serve a variety of industries. Finally, determine what you think the company’s stock is worth, subtract a reasonable margin of safety, and expect good buying opportunities.

Chapter 26: Utilities

Utilities were once considered to be conservative investments. They were preferred investments for widows and orphans because they were thought to be a safe way to generate income via dividends.

Deregulation has changed everything for this former haven. Competition in the industry will only increase as deregulation continues to expand.

Electricity Primer:

The electricity utility business can be divided into essentially three parts:

Generation: These are the companies that operate the power plants themselves: coal / natural gas / uranium in; Power off. In countries with complete deregulation, the distribution arm of the utility company often purchases electricity from external suppliers who compete with its generation arm. As competition increases and profitability decreases, it becomes more and more difficult to make a profit.

Transmission: Transmission is the business of carrying electricity over long distances, think of all high voltage / high voltage cables. Transmission companies generally have fairly large economic divisions due to the huge barriers to entry due to high upfront costs as well as NIMBY.

Distribution: Distribution related businesses own and service the final mile of the cable that carries power to individual homes and businesses. Distribution is where utilities have their greatest economic divide because they tend to have monopolies even in deregulated states with virtually no alternatives.

Regulation:

The Environmental Protection Agency (EPA) wields great power because it regulates the amount of emissions that power plants can release into the atmosphere. Anyone who owns nuclear power plants must also act under the watchful eye of the Nuclear Regulatory Commission (NRC). .

“The financial component of your leverage is far more important today. It’s easy to see why utility companies previously agreed to take on massive debt. An easy way to increase your return on equity through the use of financial leverage.”

Hallmarks of Success

Utility companies operating in states with minimal competition are much better positioned than those operating in states where deregulation has opened markets.

High liquidity and comparatively low debt are always attractive.

Companies that tried to get into industries outside of their core business tended to do much worse than firms that stayed focused. They focused on what they did best, they tended to be a lot better.