Two of the favourite topics of entrepreneurs are business growth and scaling. The words are used around a lot, but the enthusiasm with which they are used often outweighs the precision. Many people use these words to mean the same thing: a company that is getting bigger, getting more market share, and making more money. But there’s a critical difference between growing and scaling in a business sense, and it’s an important difference in understanding what really happens when businesses grow and what kind of growth to look for.

Growth in Business

When companies grow, they are increasing their revenue equally as fast as they are adding resources to enable that increase.

Scaling in Business

When companies scale, on the other hand, they add revenue at a faster rate than they take on new costs.

How to Plan for Scaling in Business

As you launch your business, you should already be thinking about a strategy for scaling your startup — not for growing. If you simply continue trying to increase your revenue by adding more resources with a corresponding increase in costs, your growth is likely to stagnate. You’ll get to a point where you realize the effort to grow simply isn’t worth the financial gain.

What you need instead is a strategy for scaling in business that focuses on increasing revenue while also increasing efficiency. In the scaling scenario, it will be worth the effort to reach more customers since you’ll be expending a comparatively low amount and therefore making increasingly large amounts of profit. You’re increasing your company’s value by increasing the efficiency with which you can bring in new revenue.

Total addressable market (TAM) slides are among the most frequently mis-executed. They are often included as a formality in an attempt to get VCs to check a mental box and continue on hearing about other important things: the product, the team, the progress, the go-to-market, etc.

TAM is the size of the market a company is catering in/planning to cater to have an idea as to the size of the market it would be sharing with its peers.

There are three methods used to calculate the total addressable market. They include:

Top-Down Approach: This method uses industry research and reports. It contains remarkably little information and relies upon secondary data comprising of facts laid out by other companies stating the size of the market without relevant data to get across those numbers. Another major pitfall here is that it assumes the company’s disruptive model won’t change the TAM meaningfully.

Bottom-Up Approach: This approach breaks down a business strategy at detailed levels. It takes the form of “here’s how we price and how many units of that price we can sell.” This is a much better option than #1, because it involves tangible, relatable data on current pricing/usage of the product and imagines a larger customer base.

Value-Theory Approach: This method uses conjecture about the buyers willingness to pay. A value-theory TAM relies on an estimate of the value provided to a set of users by the product, as well as a guess at how much of that value creation can be captured through pricing.

Saurabh Mukherjea is the Founder and Chief Investment Officer of Marcellus Investment Managers. Prior to setting up Marcellus, Saurabh was the CEO of Ambit Capital. He is a CFA charter holder with a Bachelors and Masters in Economics from the London School of Economics.

Rakshit Ranjan launched Ambit’s Coffee Can PMS in Mar’17 and managed it till Dec’18. Under his management, Ambit’s Coffee Can PMS was one of India’s top performing equity products during 2018. He holds a B.Tech degree from IIT (Delhi) and is a CFA charter holder.

Pranab Uniyal is the head (products and advisory) at Ambit Capital. He holds a BTech degree in chemical engineering from Indian Institute of Technology, Madras, and a postgraduate diploma in management from Indian Institute of Management, Calcutta.

Introduction:

Indian people have been typically Indian where the only investment tool is Gold, Real Estate and more or less “Fixed Deposit”. After these options there has been no such growth till last decade. Even in banks the Relationship Managers suggest the old ULIPs which can only be profitable to the distributor rather than the customer.

The portfolio of the Indians got limited due to three major drawbacks of the Indian Investment Pattern

The overwhelming dominance of investments such as gold, real estate, and fixed deposits. Around 88% of an Indian investor’s wealth is in these three assets.

The culture of the stock market is only two decades old. It’s relatively new compared to other countries.

And, unlike in developed countries, the Indian stock market has very few great companies that sustain over long periods.

In this book, the author has advised on how to invest for long term and perks of investing for long term through his Coffee Can Portfolio. He has explained every point with different examples step by step and in detail. Below are the key learnings from the book which one should focus on.

CHAPTER 1: MR. TALWAR’S UNCERTAIN FUTURE

Investors make some very basic investment mistakes that lead to either wealth erosion or sub-optimal returns.

The common investment mistakes every investor makes:

No clear investment plan/objective

Trading too much, too often

Lack of diversification

High commission and fees

Chasing short-term returns

Timing the market

Ignoring inflation and taxes

CHAPTER 2: COFFEE CAN INVESTING

It is interesting to know that although Sir Isaac Newton invented calculus and made ground breaking discoveries in the field of physics, he could not understand the behaviour of the market and suffered terrible losses at the time. This shows that patience is just as important when investing in stocks.

This biggest misconception in the marketplace is the saying, “To get higher returns, you need to take more risks”. This statement is partially correct when we see it in relation to various financial instruments. However, on a specific instrument; say Equity; You have the option of choosing the most efficient companies for your portfolio, which significantly reduces your risk and keeps the return constant.

A company may be selected for inclusion in the portfolio based on its economic moat it possesses. This moat should be intended to set the company apart from its competitors in the long term. A moat that has to be constantly rebuilt is not a moat.

CHAPTER 5: SMALL IS BEAUTIFUL

Over the past 2 decades, small-caps have outperformed large-caps in most large stock markets. There are two key drivers of this outperformance: smaller companies have the potential to grow their profits much faster than large companies and, secondly, as small companies grow in size they are ‘discovered’ by the stock market.

Over the recent years affluent Indians have directed savings away from real estate and towards financial system. This deepening of the financial markets is helping reduce the cost of capital in India, which in turn benefits smaller businesses disproportionately.

Whilst the scope for generating superior long term investment returns is greater with small-caps, the need for professional help is disproportionately greater.

CHAPTER 6: HOW PATIENCE AND QUALITY INTERWINE

‘Patience Premium’ is the difference between annualized returns generated by a stock or an index over any holding period compared to the return generated by the same stock or index over a one-year holding period. A positive value of ‘patience premium’ implies that the longer the holding period of the stock, the higher is the return generated from it for an investor.

‘Quality Premium’ is the difference between the annualized returns generated by a stock or a portfolio and the Sensex over a particular holding period. A positive value of the ‘quality premium’ implies that increasing the quality of the stock portfolio generates better returns for the same investment horizon.

Observation 1: The shorter the holding period, the higher the quality premium

Observation 2: A high-quality portfolio with a long holding period delivers the highest return with the lowest risk

APPENDIX 2: HOW PUNCHY CAN THE P/E MULTIPLE OF A GREAT COMPANY BE?

A large proportion of investors and analysts use various ratios to value companies by comparing their past, or with their peers. But sometimes ratios like P/E and PEG can skew the actual picture of shareholder value creation and make it look rosier than it is. The interesting thing about earnings is that not only can they be manipulated according to the whims of the management team, but they only provide information about how much profit a business can generate every year and NOT about the re-investments of those earnings necessary to keep the business running. The cash flow, on the other hand, describes clearly how much of the profit is left for shareholders.

Sugar Stocks Rally as Govt Advances Ethanol Blend Target

From 2025 to 2023 the government advanced the deadline for 20% ethanol blending in petrol.

The move can divert a sizeable amount of sugarcane to ethanol production and this should essentially bode well for sugar industry as the situation of a supply glut will automatically get addressed and will support pricing discipline in long run.

The tight supply situation in global market has pushed sugar prices to a four year high.

Max Life, Tata AIA Make Vaccination Must for Term Life

Insurance companies such as Max Life and Tata AIA have taken the lead in asking for mandatory vaccine Covid-19 vaccination certificates from the buyers of Term life insurance.

Other insurers likely to follow the suit. The move seems to be triggered by global insurers such as Munich Re and Swiss Re, the biggest underwriters of risk for domestic insurance companies.

Non vaccinated deemed as increased mortality rate.

Mandatory vaccine certificates for term cover help tighten management in anticipation of possible third wave, encourage more people to get inoculated, increase scrutiny on vaccine hesitant policyholders.

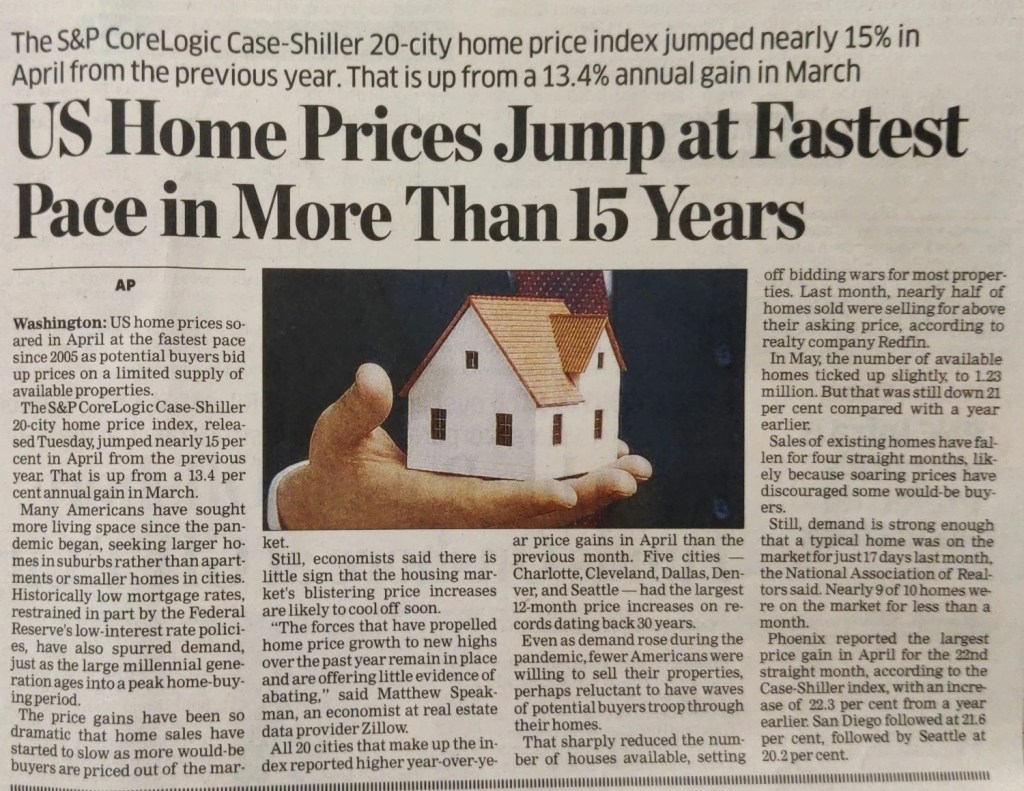

US Home Prices Jump at Fastest Pace in More Than 15 Years

US home prices have jumped at fastest pace in more than 15 years. Prices jumped nearly at 15% in April from the previous year.

As a result of the dramatic price gains the home sales have started to slow as more would be buyers are priced out the market.

All 20 cities that make up the index reported higher year-over-year price gains in April than in previous months.

Charlotte, Cleveland, Dallas, Denver and Seattle are the five cities which had the largest 12 month price increases on the record dating back 30 years.

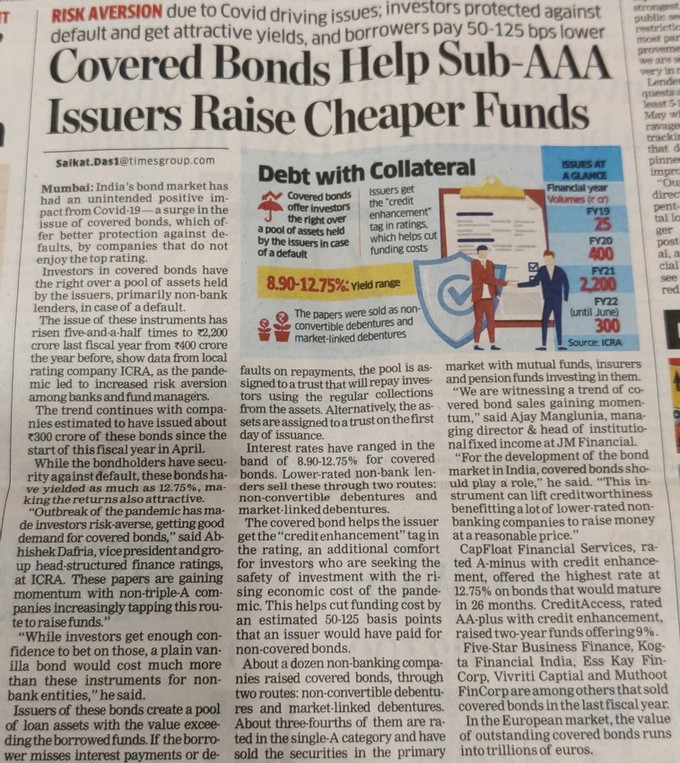

Covered Bonds Help Sub- AAA Issuers Raise Cheaper Funds

India’s bond market has had an unintended positive impact from Covid-19. A surge in the issue of covered bonds, which offer better protection against defaults, by companies that do not enjoy the top rating.

While the bondholders have security against default, these bonds have yielded as much as 12.75%, making the returns attractive

These bonds are gaining momentum with non-triple-A companies increasingly tapping this route to raise funds.

About a dozen non-banking companies raised bonds, through two routes: non-convertible debentures and market linked debentures.

Commodity Traders Bag Billions While Prices Rise for Everyone else

From oil to copper, the price of every commodity is rising in 2021. The Bloomberg Commodities Spot Index, a measure of 22 raw material prices, is up 78% from the March 2020 low when the pandemic first hit.

The world is facing a structural inflation shock. There’s a lot of pent up demand and everyone wants everything right now said Dough king.

The boom is an unwelcome development for policymakers tackling the climate crisis as rising commodities prices will make the shift more expensive.

China, reliant on raw material imports to feed millions of factories and building sites is so nervous the government has tried to force prices lower, threatening crackdowns on speculators and releasing strategic stockpiles.

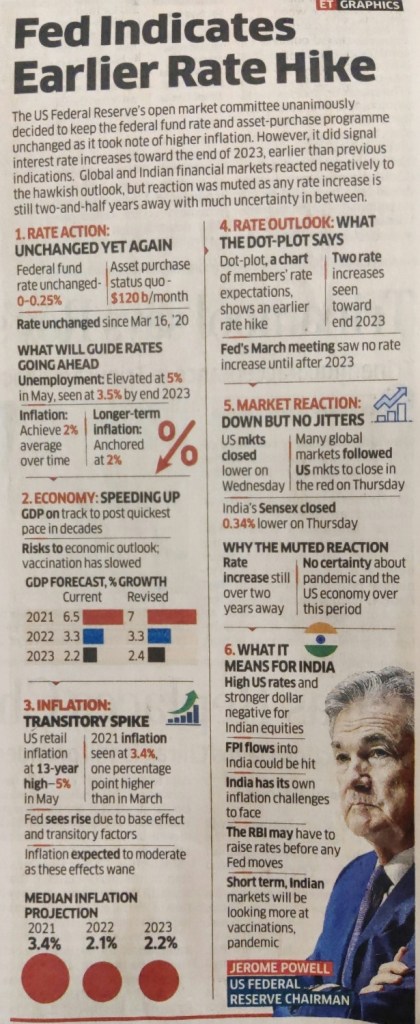

The US federal reserve’s open market committee unanimously decided to keep the federal fund rate and asset-purchase programme unchanged as it took note of higher inflation. It signalled an interest rate increase towards the end of 2023, earlier than previous predictions.

Due to the higher inflation rate the unemployment rate is estimated to be elevated from 5% to 3.5%.

Dot-Plot a chart of members rate expectations, shows a two rate hike towards end of 2023.

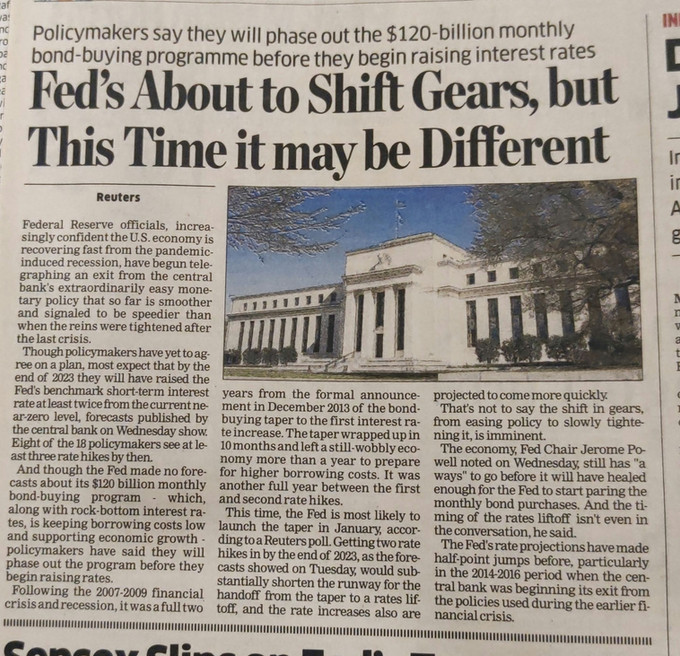

Fed’s About to Shift Gears, but This Time it may be Different

Federal Reserve officials have begun telegraphing an exit from the central bank’s monetary policy. They are increasingly confident that the U.S. economy is recovering fast from the pandemic infused recession.

By the end of 2023 they will have raised the Fed’s benchmark short-term interest rate at least twice from the net zero level.

The shift in gears, from easing policy to slowly tightening it, is imminent.

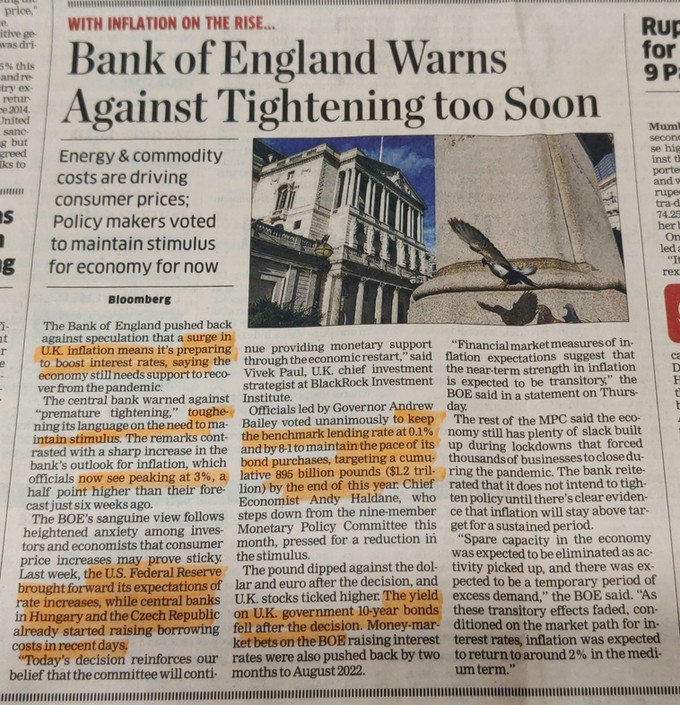

The central bank warned against premature tightening.

The inflation in England is peaking at 3%.

Hungary and Czech Republic started raising borrowing costs as these expectations came out.

Officials led by Governor Andrew Bailey voted unanimously to keep the benchmark lending rate at 0.1% and by 8-1 to maintain the pace of its bond purchases.

The yield on U.K. government 10 year bond went down.

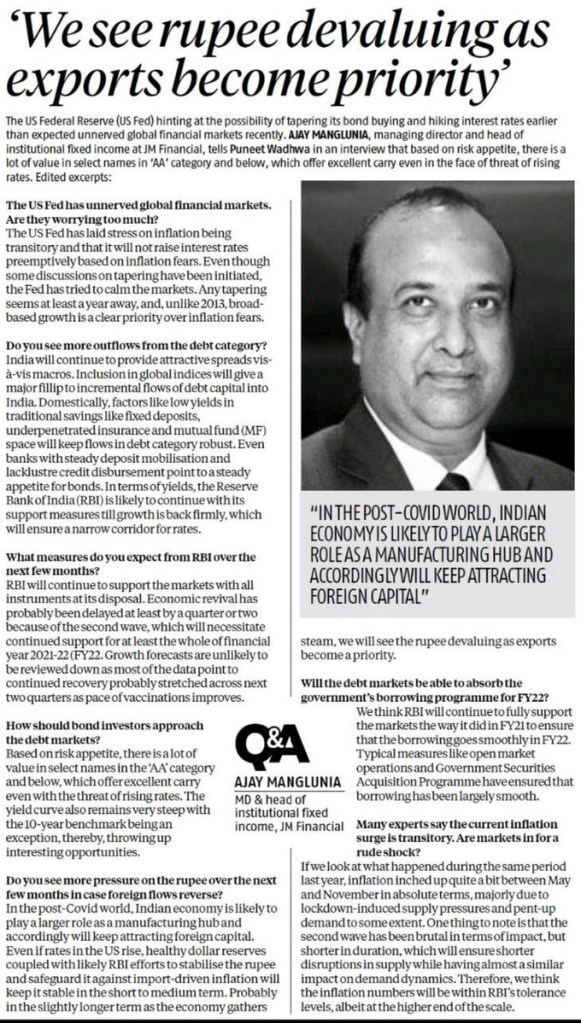

Ajay Manglunia, managing director and head of Institutional fixed income at JM Financial said in an interview that India will continue to provide attractive spreads vis-a-vis macros.

RBI is likely to continue with its support measures till growth is back firmly.

In the post-covid world, Indian economy is likely to play a larger role as a manufacturing hub and accordingly will keep attracting Foreign Capital.

Rupee will depreciate in long run as export will become a main priority for India.

The inflation will be within RBI’s tolerance levels, albeit at the higher end of the scale.

Every company tracks certain success metrics. This is a generally accepted criterion for the health of a business. But speaking of markets, these measures are often inaccurately defined or confused in interpretation. Of course, the benchmarks are also different as the markets differ significantly in product categories and customer bases. However, the following list should serve as a primer on the key indicators that the creators of the marketplace need to know to tune their performance and evaluate their future potential.

The following are the 13 metrics for marketplace companies:

Match Rate

Market Depth

Inventory Turnover

Concentration or Fragmentation of supply and demand

Metrics are measures that are used to monitor and evaluate all the different parts of a business. Good metrics aren’t just about raising money from VCs … they’re about running the business in a way where founders can know how — and why — certain things are working (or not), and then address them accordingly. In other words, metrics aren’t just for pitching but for discussing in subsequent board quarterly updates, and management meetings. “Drive with them, don’t just ‘report’ them”.

The following metrics are important to track in startups:

Business and Financial Metrics

Bookings vs. Revenue

Recurring Revenue vs. Total Revenue

Gross Profit

Total Contract Value vs. Annual Contract Value

Life Time Value

Gross Merchandise Value vs. Revenue

Unearned or Deferred Revenue… and Billings

Cost Acquisition Cost… Blended vs. Paid, Organic vs. Inorganic

Total Addressable Market

ARR ≠ Annual Run Rate

Average Revenue Per User

Gross Margins

Sell-Through Rate & Inventory Turns

Cumulative Charts

Product and Engagement Metrics

Active Users

Month-on-month

Churn

Burn Rate

Downloads

Presenting Metrics Generally

Cumulative Charts (vs. Growth Metrics)

Chart Tricks

Order of Operations

Truncating the Y-Axis

Economic and Other Defining Qualities

Network Effects

Virality

Economies of Scale

Other Product and Engagement Metrics

Net Promoter Score

Cohort Analysis

Registered Users

Active Users

Source of Traffic

Customer Concentration Risk

Checking metrics is almost like doing a health check for your baby at the pediatrician’s office. Check weight and height, and then compare to previous estimates to make sure things look healthy before you go any deeper!

What is meant SAAS? – SAAS stands for Software as a service. SAAS companies are the companies that use software to provide service to their customers. There are two main Software as a Service (SaaS) metrics that can help pave the way to profitability. It is the customer acquisition cost (CAC) ratio and the customer lifetime value (CLTV).

Customer Acquisition Cost (CAC) Ratio:

The customer acquisition cost (CAC) ratio is a comparison of two factors: the total sales and marketing costs associated with acquiring new customers and the incremental increase in gross profit on new customers over a specified period of time.

CAC Ratio= Annualised Gross Profit / Sales and Marketing Expenses

The calculation uses gross profit and not revenue because gross profit is what you really earn from a customer by selling your product after deducting its cost.

Customer Lifetime Value CLTV Ratio:

Customer lifetime value (CLTV) is, on average, the total revenue expected per customer. In other words, CLTV is an estimate of the average customer’s total subscription value. As the name implies, CLTV measures the overall lifetime value of a customer.

CLTV= Average Revenue Per Account (ARPC) x Average Customer lifetime

Disruption is a fundamental change to an existing industry or market by technological innovation leading to a path never explored until now.

The four stages of disruption are:

Disruption of the incumbent- A new product, technology, or service may be recognized as different and replace an existing widely used product, technology or service.

Rapid and linear evolution- While focusing on retaining customers that have been acquired, incumbents try to control the situation by commenting on a new product, technology, or service as a vague or very easily achievable set of tasks.

Appealing Convergence- The market begins to recognize the importance and use of new products, technologiesand services and begins to switch to them.

Complete reimagination: The disruptor analyses the strengths and weaknesses of products, technologies, and services in existing markets, considers and merges key aspects of products, technologies, and services, and implements them in an attempt to create a completely new upgraded category.

From the outlook of an incumbent:

You need to analyse whether your competitors are disruptive. And have to analyse what they have to offer, is it more than what we offer?

From the outlook of the disruptor:

An important decision to make is when and how to use convergence.

Be prepared for new disruptors to come in and seize the market.

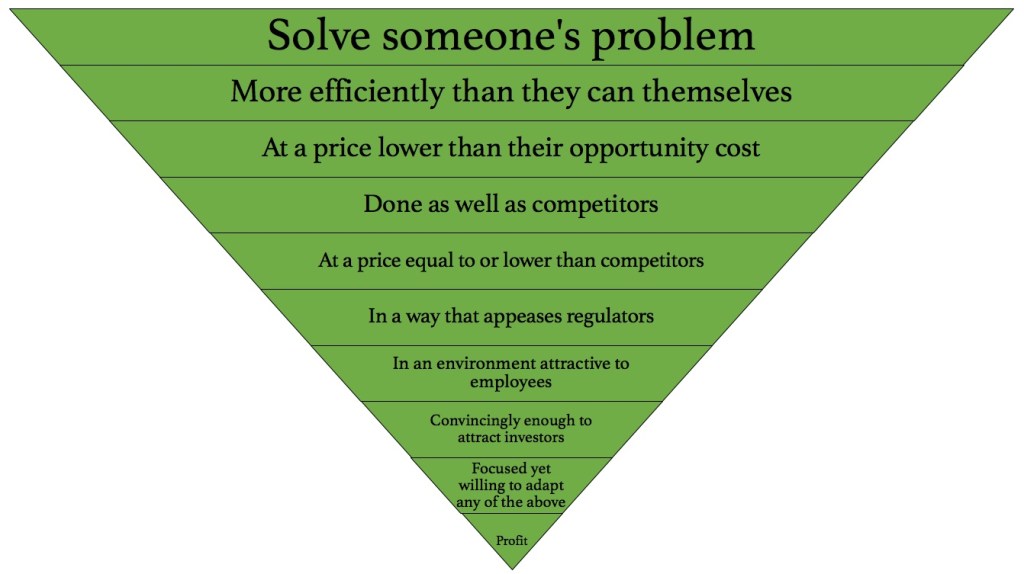

Morgan Housel is a partner at Collaborative Fund and a former columnist at The Motley Fool and The Wall Street Journal. He states that the gap between a great product and a great business can be ten miles wide.

We need to know what a Product and Business simply means:

A product is something that can solve someone’s problem.

A business is a product that serves so works so well that people will pay more than it costs to produce.

All great businesses are backed by great products, but not all great products turn into great businesses, so it’s important to separate the two different things.

A product can be great if it lives in the top few boxes of the pyramid. Getting from there to the bottom is incredibly hard. Figuring out how to make a business work means running losses for a period of time. But losses incurred to build tomorrow’s infrastructure are different loses incurred because it can’t charge the customers a price that reflects what it costs to run the business.

The best way to achieve the vision of building a company that will last for generations is to build a good business with the same passion as making a good product. And that strategy needs to be implemented early on to the last generation in the business. And it has nothing to do with losing the focus of the product.

Fifty years ago, the answer to what a technology company was a simple question. IBM was a technology company and everyone else was a customer of IBM. It may have been a little exaggerated, but not by much. When asked today, what is a tech company, the answer will probably be that the company whose business model is structured around technology, to build and improve technology or make advanced contributions in the field of AI is a tech company.

In the initial years when the world of technology was not very advanced and the use of software was not popular, the applications of technology companies were widely related to hardware. The only dominant player in this technology was IBM.

IBM provided services including building, training and ongoing maintenance of the hardware, including operating systems and applications, custom business software. All kinds of industries have been customers of IBM technology. IBM has been a complete ecosystem in its own right, but after that, it became hard to manage all the hardware, software, services, etc.

IBM therefore began outsourcing its software division to Microsoft. In 1980, when software licensing was introduced, Microsoft separated the software business from the hardware business by charging every copy without selling or servicing the basic running hardware. Silicon Valley then started garnering attention because these software companies had capital requirements for the initial development process after which the costs were negligible for manufacturing an endless amount of chips. This made Venture Capitalists go for these start-ups as they could earn ‘an infinite pool of returns’ if they were successful.

The basic characteristics to define a tech company: